Popping the residential housing bubble brought dramatic change to the levels in residential construction and the industries tied to it. Fein is predicting mild recovery in 2010.

“There is really no easy way to put this, it was really bad. Almost as bad, although not quite exactly as bad as the fourth quarter of last year, but nearly as bad.”

As compared to first quarter 2008, Fein showed a 14.9 percent decrease of actual revenue and an 18.9 percent decrease of real revenues for the hardware, plumbing, and heating equipment/supplies wholesaler sector. According to the report, real revenue equals actual revenues adjusted for product inflation using sector-specific price deflators. The building material and construction wholesale distributors sector’s actual revenue was down 23.5 percent and its real revenues were down 26.2 percent. Overall, the entire wholesale distribution industry experienced a 17.2 percent drop in first quarter actual revenues, and a 9.5 percent decrease in real revenues.

“The most volatile sectors were oil and gas products, metal service centers, and agricultural products wholesale distributors,” pointed out Fein. “But, for a number of these sectors, the deflation - the popping of the commodity bubble - made these numbers look a lot worse.”

POPPING THE BUBBLE

The causes for this downturn have been discussed at length among economists across the nation. One of the greater contributing factors is the popping of the residential housing bubble. The significant growth occurring primarily in 2005 and 2006 brought about a quick building pace and exponentially increased profits. At the peak, builders were constructing 2 million new homes/housing units a year.“That was far above what the market could absorb and it is going to take a long time, if ever, to get back to that level,” said Fein. “We are in what is probably the first and most significant housing led downturn of the modern era and the excesses of this housing boom - the biggest credit and asset bubble in U.S. economic history - are going to take years to resolve.”

Addressing economic resolutions, Fein discussed three distinct patterns of recovery for the distribution industry and the American public to watch for - V-, U-, and L-shaped.

V-shaped recovery is a quick recovery. It begins with a long hard drop that hits the bottom and starts back up again with a steady growth pace. U-shaped recovery is much the same, but slower. It takes the same dive to the bottom, lingers there briefly and steadily, and then begins back towards the top.

“The problem with V-shaped recovery is there’s a probability of very significant levels of inflation,” said Fein. “We have extraordinary levels of monetary stimulus. Most of the fiscal stimulus will not be hitting until next year, just as the economy is getting warmed up. A large amount of money in the market, coupled with massive amounts of U.S. debt, threatens potential devaluation of the U.S. dollar.”

Fein cautioned his audience that a quick recovery in 2010 could lay the groundwork for incredibly high inflation, “or, to give you a nightmare scenario to contemplate, we return to the 1970s, early ’80s where we need to raise interest rates to control this inflation and we end up in a type of double dip recession.”

Because of this, Fein is hoping for a U-shaped recovery. It is slower, steadier, and the end result is a distinct return to profitability.

The L-shaped recovery is one model that most likely everyone is hoping to avoid. This model shares the significant plunge to the bottom, just as in the U- and V-shaped models, but after that it levels off and the bottom becomes the new normal. Fein gave the example of Japan in the 1990s to prove his point.

With these recovery models in mind, distributors are faced with preparing and structuring their businesses to weather the financial lulls and storms that are on the unpredictable horizon.

“There is a vast amount of volatility and some brand new risks that are popping up,” warned Fein. “I would say that this is the time when, more than ever, you need to be prepared to understand what’s going on sooner, because we are entering some very choppy waters, even though it looks like the recovery is getting going.”

A 14.9 percent decrease of actual revenue and an 18.9 percent decrease of real revenues for the hardware, plumbing, and heating equipment/supplies wholesaler sector made for a tough first quarter.

STABILITY DENOTES IMPROVEMENT?

National reports have already begun the talk of the improving economy. Stated often in local and national media, it is the opinion of many that the economy has seen the worst and is now headed towards an upswing. Some economists agree, but there are others that feel the general population should not be as relieved as certain politicians are saying they should be.Fein’s presentation gave attendees the comfort that things are becoming stable once again, but warned that it would still take time for actual improvement to be experienced.

Two of the multiple indicators that he said to watch for are consumer confidence levels and unemployment rates. According to the Conference Board Survey, a consumer confidence survey that has been conducted every month since the 1960s, consumer confidence is bouncing off historic lows. Coupled with a new saving money trend, a lot of dollars are not being spent, effectively slowing improvement.

“If consumers save at a rate of 5 percent as opposed to the current 0 percent, you remove trillions of dollars from the economy,” said Fein.

Employment rates are good indicators as to how much actual improvement is registering in the economy, too. Current numbers in- dicate the national unemployment rate to be above 9 percent, and Fein is predicting it will likely be over 10 percent by the end of the year.

“There are almost 14 million people considered right now to be officially unemployed, and it is going to take quite a while to reabsorb those people back into the workforce,” he said. “Total employment in distribution has declined at a slightly faster rate than the overall economy, particularly in sectors related to building materials, which just in this recession alone has lost almost one-fifth of all its workers.”

According to Fein, distributors should keep an eye on the number of hours worked posted by companies. “Before companies start adding jobs, they traditionally add more hours first,” he said. “We definitely see right now some signs of stability, and we find that when you look forward into the quarter-to-quarter growth comparing to the previous year, we see some stability in that and the expectation that the next year, for a variety of reasons, looks a lot better.”

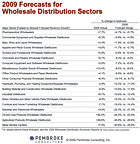

The forecasted revenue range for the hardware, plumbing, and heating equipment/supplies wholesalers sector for 2009 is a decrease of 11 to 12 percent as compared to the 4.9 percent decrease of 2008.

CONSULTING CRYSTAL BALLS

“If you make your living predicting the future and you use a crystal ball, every once in a while you have to eat glass,” Fein laughed as he explained that his predictions weren’t always correct. But, in his years of experience, he is often correct in what the research reveals. As for the future of the HVAC distribution industry, Fein’s research shows “pretty dramatic revenue declines in most of the distribution sectors.”Last year’s decline for the hardware, plumbing, and heating equipment/supplies wholesalers totaled 4.9 percent. The forecasted range for 2009 is a decrease of 11 to 12 percent.

“I think what we are seeing, at least my expectation now, is that we are kind of troughing out and the expectation after this is slow and steady recovery going forward,” said Fein. “Again, I would say that this is the most likely scenario, but it is not the only scenario out there.”

For more information, visit www.naw.org. Adam Fein’s “2009 Wholesale Distribution Economic Reports” along with his “Outlook 2009” are available there.

Publication date:07/20/2009