In the first installment, we discussed how the values of contracting businesses have come full circle in approximately six years. With an inactive acquisition market (due to the exodus of actively acquiring consolidators), there is a renewed opportunity for contractors to expand their businesses by acquiring all or part of a competitor’s business at price levels and terms that realistically correlate to the risks and rewards associated with a transaction. In this article, I will outline a few key areas to consider when formulating purchase price.

Why Are You Buying?

Prior to making contacts with a prospective acquisition, one should first gain an understanding as to why an acquisition is the best course of action to take. There are several reasons, but more than likely the purpose will be to expand your existing customer base with the goodwill of the business you are buying.For the purpose of this article, goodwill is defined as the acquired company’s name, reputation, customer list, customer database, Yellow Pages placement, and telephone numbers. As easy as goodwill is to define, it can be complicated to value due to the fact that it is intangible. Unlike service vans and tools, which are tangible, one can’t accurately estimate the value of a customer list by checking for rust, dings, and bald tires.

Historical Income Statements

Although there has been changes in the way contracting businesses are valued, what remains constant is the reliance upon historical financial statements (income statement and balance sheet). Historical income statements are the cornerstone of the valuation process due to the fact that the past is typically and accurate prediction of the future. Without at least three years of financial statements to analyze, it is impossible to gauge the value of a business and how the purchase of that business will help to benefit the future earnings of your company.In addition to historical income statements, it is important to visit with the candidate and gain an understanding of the targeted business. What may appear to be an excellent fit into your business from afar may quickly change once you have had the opportunity to obtain additional information. You may be seeking to expand your commercial HVAC service business and quickly discover your candidate performs significantly less commercial work than you had thought. In such a case, you chose to look no further into that prospect.

Valuation Approaches

Analyzing and adjusting the historical financials will indicate the profitability of the business. This is a crucial point, as a non-profitable business is typically valued differently than a profitable business. It is fair to say that a business that shows a continual lack of profitability will have goodwill of little or no value. Yes, this business will have some fixed assets, but if you are looking to acquire future benefits from the goodwill, look elsewhere.One exception being that you may be able to convert some of the customers into profitable customers, but do so only if you are confident that the rewards far outweigh the risks. Finally, the value of a non-profitable business’s assets can materially vary based on their ongoing operation (or lack thereof) and the condition of the assets.

Profitable businesses should be valued in a different manner. The value of goodwill increases as the earnings of the business grow. I’ll explain.

All businesses have assets and most have at least some liabilities. To purchase the assets requires a commitment of capital, which if invested elsewhere, would produce a return (assume 10 percent in this example). The goodwill earnings become the difference between the expected return on the assets if invested elsewhere and the total earnings. Example, assuming you are contemplating the acquisition of a four-truck residential service and repair HVAC business with $650,000 in revenues and 10 percent adjusted pre-tax income. Further assume that the business’s assets have a replacement value of $75,000 and total liabilities of $25,000.

Total Assets – Total Liabilities = Net Assets

$75,000 - $25,000 = $50,000

Net Assets x Expected Percentage Return On Assets = Expected Dollar Return On Assets

$50,000 x 10% (0.10) = $5,000

In this example, the expected return in dollars on the net assets is $5,000. Pre-tax earnings over $5,000 are considered goodwill earnings.

Total Earnings - Expected Dollar Return On Assets = Goodwill Earnings

$65,000 - $5,000 = $60,000

The goodwill earnings of $60,000 are key to the valuation of this business. What the buyer ultimately will pay for the earnings is based upon the capitalization rate, a subjective rate of return on the investment. The capitalization rate is calculated subjectively taking into consideration several factors including:

What Is Its Value?

Acquiring and maintaining the goodwill earnings of a competitor is risky and all risks should be considered. Many buyers within the trades have discovered that if not properly integrated, the benefits of acquiring customer lists, databases, telephone numbers, and names quickly vaporized. Unfortunately, integrations of a newly acquired business are beyond the scope of this article.Regarding the example above, while it is clear that net assets have a value of $50,000, the combined value (net assets plus goodwill value) will have a range contingent upon the factors outlined above. Taking these factors into consideration, the investment value could vary widely, but for a company of this size, the fair market value would range between $170,000 and $221,428. The investment value, the value of which an investor taking into account these synergies would pay, may actually exceed $221,428 depending on his or her estimated risks and rewards. However, a buyer should be strongly cautioned not to underestimate the risks and overestimate the rewards.

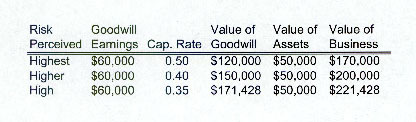

The value of the goodwill is determined by dividing the goodwill earnings by the capitalization rate. The capitalization rate varies from one business to another. As demonstrated in the chart above, as the perceived risk rises, the capitalization rate increases and the value of the goodwill earnings decreases.

The valuation of any business requires the application of both art and science. Additionally, there are certainly many more methods that may be utilized other than the one demonstrated in this article. Furthermore, as the size of the targeted business decreases, the risk associated with the goodwill increases substantially, further reducing the value.

In conclusion, what is important to know is that the risk associated with acquiring a business must be offset by the expected rewards. Both private and public buyers within the trades have demonstrated that the risk factors associated with acquisitions are high. With that being said, when analyzing an acquisition target, evaluate all aspects of the transaction to confirm that the rewards outweigh the risks. If you cannot convince yourself this is the case, don’t complete the transaction.

Brandon Jacob has been active in acquiring contracting businesses for over six years. He has prospected, analyzed, valued, and negotiated acquisitions for ARS and ARS/ServiceMaster. Jacob is a CPA, a Service Roundtable Consult & Coach Partner, and currently assists contractors in all aspects of mergers and acquisitions and business valuations projects. He can be reached at 713-426-4041 or BGJacob@aol.com.

Publication date: 06/02/2003